Putting a price on pain and suffering is one of the most challenging parts of a personal injury claim. Unlike a stack of medical bills, emotional distress doesn't come with an invoice. So, how do you translate something so intangible into a dollar amount?

It’s not about guesswork. Courts and insurance companies rely on established methods to bring some objectivity to a subjective experience. The two most common approaches are the multiplier method and the per diem method. These aren't perfect, but they provide a logical starting point for negotiations.

Framing Your Emotional Distress in a Personal Injury Claim

After an accident, the physical injuries are often just the tip of the iceberg. The real, lasting damage can be psychological—the anxiety that keeps you up at night, the depression that drains your energy, or the PTSD that makes everyday life feel like a minefield. This is what we call emotional distress in a legal context.

As a "non-economic" damage, emotional distress compensates you for the kind of suffering that doesn’t have a clear price tag. But to get that compensation, you can't just say you've been feeling down. You have to build a case.

The Foundation of an Emotional Distress Claim

The core of any successful claim is proving a direct link between the other party's negligence and your psychological suffering. This isn’t about just feeling sad; it’s about demonstrating a measurable decline in your mental health and quality of life because of what happened.

This evidence needs to be specific and well-documented. We’re talking about things like:

- Anxiety or panic attacks that weren't there before the incident.

- Diagnosed depression or profound mood swings that strain your relationships.

- Post-Traumatic Stress Disorder (PTSD), complete with flashbacks, nightmares, and avoidance behaviors.

- Loss of enjoyment of life—the inability to engage in hobbies, sports, or activities that once brought you joy.

Your personal story is powerful, but it's the professional documentation that gives it legal weight. That's how you turn a subjective experience into a strong argument for the compensation you deserve.

For instance, if you were in a car crash, seeking out resources like ICBC counselling after an accident is a critical step. Not only does it help you heal, but it also creates an official record from a mental health professional, which is invaluable for substantiating your claim.

The whole valuation process can be visualized as a straightforward path: the injury happened, we apply a structured calculation to it, and we arrive at a final value for your claim.

This flowchart shows how we move from the initial event to a concrete number used in settlement talks. Each stage requires solid evidence and a compelling narrative to justify the final figure.

Emotional Distress Calculation Methods at a Glance

To make this clearer, let's break down the two main calculation methods you'll encounter. Each has its own logic and is better suited for different types of cases.

| Method | How It Works | Best Suited For |

|---|---|---|

| The Multiplier Method | Total economic damages (medical bills, lost wages) are multiplied by a number from 1.5 to 5. The multiplier depends on injury severity. | Cases with significant, long-term, or permanent injuries where the emotional impact far exceeds the initial economic costs. |

| The Per Diem Method | A daily dollar amount ("per diem") is assigned for each day of suffering, from the accident date until maximum recovery. | Shorter-term, straightforward recovery periods where the duration of pain and suffering is clearly defined and finite. |

Ultimately, choosing the right method—or sometimes a blend of both—is a strategic decision. It depends entirely on the specifics of your injury, the strength of your evidence, and the long-term impact on your life.

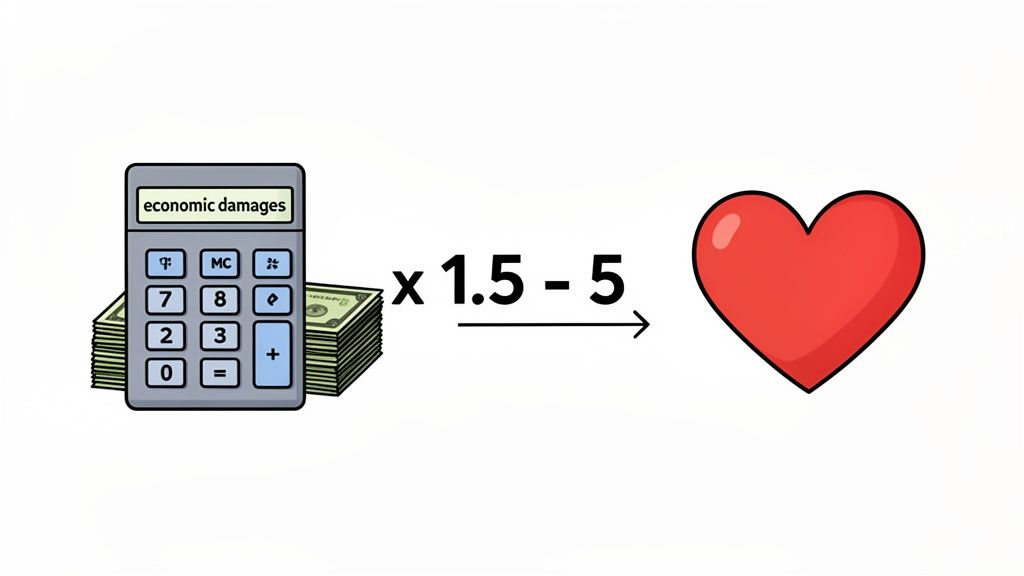

Applying the Multiplier Method to Your Economic Damages

When it comes to putting a number on emotional distress, the multiplier method is often the go-to starting point for attorneys. It’s a workhorse in personal injury law because it creates a clear, logical bridge between your hard financial losses and the very real, but intangible, suffering you’ve endured.

The whole process kicks off with a detailed accounting of your economic damages. This isn't just a quick tally; it’s a meticulous, line-by-line calculation of every provable expense and loss stemming from the injury.

Establishing Your Base Number

This foundational figure, sometimes called "special damages," is what the rest of the calculation hinges on. Before you can even think about a multiplier, you need a rock-solid, fully documented total. This base number should capture everything, including:

- Medical Bills: From the first ambulance ride to ongoing physical therapy, prescriptions, and follow-up appointments—every single bill counts.

- Lost Wages: The income you couldn't earn because your injuries kept you out of work.

- Future Lost Income: A crucial piece if the injury has permanently impacted your ability to earn a living down the road.

- Property Damage: The cost to repair or replace your car, phone, or any other property damaged in the incident.

- Out-of-Pocket Expenses: All those other costs that add up, like travel for medical care or necessary home modifications.

Let’s walk through a quick example. Say you were in a slip-and-fall accident, and your economic damages came to a total of $25,000. This figure covers your hospital stay, surgery, six weeks of lost wages, and the course of physical therapy. That $25,000 is your base number, the concrete figure we'll use to calculate your emotional distress.

How to Select an Appropriate Multiplier

Once you have that base number nailed down, the next step is to select a multiplier. This figure, which usually falls somewhere between 1.5 and 5, is where the severity of your pain and emotional trauma enters the equation.

Choosing the right multiplier isn't guesswork. It's about accurately reflecting how profoundly the injury has impacted your life.

A lower multiplier—think 1.5 to 2—is generally used for injuries that heal without major long-term complications. For instance, a simple broken arm might cause a few months of pain and inconvenience but doesn't fundamentally change your life or lead to chronic anxiety.

On the other hand, a higher multiplier of 3 to 5 is reserved for catastrophic, life-altering injuries. This is for cases where the emotional toll is severe and permanent. A traumatic brain injury resulting in personality changes, deep depression, and the loss of a career you loved would absolutely justify a multiplier on the higher end of that scale.

The multiplier method isn't just about a math formula. It's about using that formula to tell a compelling story—a story that is backed by hard evidence. The multiplier you choose must be directly tied to the proof of your suffering.

Across the U.S., this method is one of the most common ways to value a claim. In fact, insurance industry data shows that 65% of personal injury settlements that account for emotional distress use a multiplier between 2 and 4. This range often represents a middle ground between a victim’s actual losses and what an insurer might see as a reasonable payout. You can explore more about typical settlement amounts on 1800thelaw2.com.

Justifying a Higher Multiplier in Your Claim

You can bet an insurance adjuster is going to push back on a high multiplier. If you’re arguing for a multiplier of 3, 4, or 5, you need to come prepared with compelling proof that demonstrates just how significantly your quality of life has diminished.

Here’s the kind of evidence that strengthens your case:

- Severity and Permanence: A permanent disability or disfiguring scar will always carry more weight than a temporary injury.

- Intensity of Pain: Chronic pain that requires long-term management is a very powerful factor.

- Impact on Daily Life: Can you no longer enjoy your hobbies, play with your kids, or handle simple household tasks? This is crucial.

- Mental Health Treatment: A documented diagnosis of PTSD, anxiety, or depression from a qualified therapist or psychiatrist is essential.

- Disrupted Relationships: Testimony from family and friends describing how your personality has changed or how relationships have been strained can be incredibly persuasive.

Let’s go back to our slip-and-fall case with $25,000 in economic damages. The difference a multiplier makes is stark:

- With a 1.5 multiplier: The emotional distress portion would be $37,500.

- With a 4 multiplier: That same portion jumps to $100,000.

This massive gap shows why fighting for the right multiplier is so critical. While emotional distress and pain and suffering are closely related, they are distinct legal concepts. If you're looking for more detail, our firm has a guide that breaks down how to calculate pain and suffering damages specifically. A well-built claim will use the full weight of the evidence to justify the highest possible multiplier, ensuring the final compensation truly reflects the depth of your experience.

Putting a Daily Value on Your Suffering: The Per Diem Method

If the multiplier method feels a bit too broad, there's another approach that takes a more granular, day-by-day look at your ordeal: the per diem method. In Latin, "per diem" simply means "per day." The entire strategy revolves around assigning a specific dollar amount for each day you had to endure pain, anxiety, and distress because of your injury.

Think of it as putting a price tag on a day of suffering. The argument is that every single day you lived with the fallout from an accident—from the moment it happened until you were as recovered as you were going to get—had a real, quantifiable cost to your quality of life. This gives you a clear, logical way to build your emotional distress claim from the ground up.

How Do You Justify a Daily Rate?

Here's where the rubber meets the road. You can't just pull a number out of thin air; an insurance adjuster will dismiss it instantly. The most common and defensible strategy is to anchor your per diem rate to your daily earnings.

The logic here is powerful and easy to understand: if a regular day of your time and labor is worth a certain amount, then a day spent suffering and unable to live your life should be worth at least that much. For example, if you earned $240 per day at your job, that figure becomes a solid, reasonable starting point for your daily rate of suffering.

By grounding your claim in a verifiable number like your income, you make it much harder for the other side to argue that you're just being emotional or exaggerating your claim.

Calculating the Total Value

Once you've settled on a justifiable daily rate, the next step is calculating the duration. This isn't arbitrary; the clock starts on the date of the incident and stops the day your doctor says you've reached Maximum Medical Improvement (MMI). MMI is the point where your condition has stabilized, and you're not expected to get any better.

The formula itself is incredibly straightforward:

(Daily Rate) x (Number of Days of Suffering) = Total Emotional Distress Damages

Let's walk through a real-world scenario. Say you were in a car accident that resulted in a broken leg requiring surgery. Your doctors tracked your recovery, and it took 210 days to reach MMI. If your daily income was $200, the math would look like this:

- $200 (Daily Rate) x 210 (Days of Suffering) = $42,000 (Total Per Diem Damages)

This method provides a precise valuation of your emotional distress. It’s particularly effective for injuries with a clear recovery timeline. In fact, one study that reviewed 500 settlements found the per diem method was used in 30% of claims involving ongoing therapy, as it helps capture the true cost of a prolonged recovery. You can find more practical insights on calculating injury settlements at HeardLawFirm.com.

When Does the Per Diem Method Work Best?

This strategy isn't a one-size-fits-all solution. It truly excels in specific situations.

- Injuries with a Clear Healing Timeline: Think broken bones, surgical recoveries, and other conditions that have a generally accepted medical recovery window.

- Cases with Meticulous Documentation: Your success here depends on your records. You absolutely need medical documentation to prove the start and end dates of your recovery.

- Claims Involving Temporary Disability: If an injury kept you from working or living your normal life for a defined period, the per diem method lines up perfectly with that timeframe.

Key Takeaway: The per diem method is compelling because it's simple and logical. But its power is directly tied to how well you can justify both the daily rate and the number of days you're claiming.

You can bet an insurance adjuster will push back on both figures. They'll argue your rate is too high or that you should have recovered faster. This is why your evidence is non-negotiable. Back up your medical records with personal journals detailing your daily struggles, notes from your therapist, and even statements from family and friends who witnessed what you went through. This builds a powerful, multi-layered case that substantiates the true duration and severity of your suffering.

Backing Up Your Number: How to Prove Your Emotional Distress Claim

Putting a number on emotional distress is one thing; proving it is another. Without solid evidence, your calculation is just a number on a page. To get an insurance adjuster—or a jury—to take it seriously, you have to show them the real-world impact of your suffering.

This is where you build the foundation of your claim. It’s not enough to just say you’ve been suffering. You need to paint a clear picture of your life before the incident and compare it to your life now. The goal is to draw an undeniable line connecting the defendant’s negligence directly to your pain and suffering.

Your Medical and Mental Health Records Are Crucial

When it comes to proving emotional distress, the most persuasive evidence comes from medical and mental health professionals. Their reports and treatment records turn your personal experience into objective, verifiable facts that are tough for an insurance company to ignore.

A vague claim of "feeling anxious" won't get you very far. A formal diagnosis from a licensed provider? That’s a different story.

Here's the core medical evidence you'll need to gather:

- Formal Psychiatric and Psychological Evaluations: This is the cornerstone. A diagnosis of a specific condition like Post-Traumatic Stress Disorder (PTSD), a major depressive disorder, or a generalized anxiety disorder from a qualified expert gives your claim immediate credibility.

- Therapy and Counseling Records: Notes from your sessions with a therapist, counselor, or social worker create a detailed timeline. They show your commitment to getting better and document your specific struggles over time.

- Prescription History: A record of medications prescribed to manage your mental health, like antidepressants or anti-anxiety drugs, is powerful proof. It demonstrates that your symptoms were severe enough to require medical intervention.

Collecting these documents is only half the battle. You have to organize them so they tell a clear, compelling story. For a step-by-step guide on this, check out our article on how to organize medical records. Once everything is in order, you can start extracting key insights. Understanding what is document analysis can help you pull the most impactful information from these dense files.

Don't Underestimate Your Own Story

While expert reports are vital, your personal account brings the human element to your claim. Nothing makes your suffering more real than your own words, written in the moment. Keeping a personal journal is one of the most effective things you can do.

Think of it less as a diary and more as a detailed log of your new reality. Be specific.

- Track your daily symptoms: Note the intensity of your anxiety, the frequency of flashbacks, or your general mood. Use a 1-10 scale if it helps.

- Log sleep problems: Did you have nightmares? Did you lie awake for hours? Write it down.

- Detail the impact on daily life: Record every time you had to skip a social event, couldn't focus on a hobby you once loved, or struggled with simple household chores.

- Note the strain on relationships: How has your emotional state affected your interactions with your spouse, kids, friends, or even coworkers? Be honest.

This isn't just venting; it's evidence creation. A consistent, contemporaneous journal transforms abstract terms like "anxiety" into a concrete, day-to-day struggle that an adjuster can’t easily dismiss.

Bring in Witnesses to Vouch for You

You're not the only person who has seen how this incident changed you. Testimony from people who know you well provides powerful, third-party validation for everything you're claiming.

Statements from your family, close friends, or even a trusted manager at work can be incredibly persuasive. They can talk about the person you were before the accident and contrast it with the person you've become.

For instance, your spouse can testify about your withdrawal or new irritability. Your boss could speak to a noticeable drop in your work performance and focus. Together, these voices create a 360-degree view of your suffering, making your claim for emotional distress damages that much stronger.

How Real-World Factors Influence Settlement Values

Putting a number on emotional distress isn't about plugging figures into a simple formula. In the real world, a handful of key factors can dramatically shift the final settlement value. It’s absolutely essential to understand these variables to build a strong negotiation strategy and set realistic expectations.

Think about it: a claim for some temporary anxiety after a minor fender-bender is a world away from a case involving debilitating, long-term PTSD from a catastrophic event.

The two biggest drivers of value are, without a doubt, the severity and duration of your suffering. Distress that clears up after a few months of therapy will always be valued lower than a condition that permanently changes your ability to work, socialize, or just enjoy your life. Insurance adjusters and juries need to see tangible proof of this impact, which is why consistent, thorough documentation is non-negotiable.

The Defendant’s Conduct and Your Case's Jurisdiction

The story behind the injury matters immensely. Was the incident a simple, careless mistake? Or was it the result of gross negligence or even intentional malice? A jury will almost always award a higher amount for emotional distress when the defendant’s behavior was particularly reckless or outrageous.

Where your case is filed is another critical piece of the puzzle. State laws on non-economic damages are all over the map. Some states put strict caps on what you can recover for emotional distress, while others have no limits at all. Even the general attitude of juries in a specific county can influence how these claims are valued.

Your Credibility Is Your Currency

It might not seem fair, but your personal credibility and how you come across can make or break your claim. Insurance adjusters and jurors are human. If they see you as honest, consistent, and sympathetic, they're far more likely to value your suffering fairly.

On the flip side, inconsistencies in your story or any hint that you're exaggerating your symptoms can do serious damage. This is precisely why keeping a detailed, honest journal and giving consistent accounts to all your medical providers is so important.

The narrative of your claim is built on more than just calculations. It’s a combination of documented suffering, legal precedent, and human perception. Each element must be strong to support the value you’re seeking.

Recent data shows just how wide the range in settlement values can be. Cases involving moderate anxiety or depression that require therapy often settle between $30,000 and $75,000. However, severe PTSD cases can easily surpass $100,000, and claims involving intentional infliction of emotional distress (IIED) might reach $500,000 or more. These figures have seen a 35% increase over the last decade, reflecting a greater societal understanding of mental health. For a deeper dive, you can learn more about emotional distress damage calculations and trends.

Seeing the Impact in a Hypothetical Case

To make this more concrete, let's look at a hypothetical case where the economic damages—medical bills and lost wages—total $20,000. The table below illustrates how different real-world factors could dramatically change the final settlement.

How Key Factors Impact Emotional Distress Settlement Value

| Scenario Factor | Impact on Calculation | Potential Settlement Range |

|---|---|---|

| Minor Negligence | A low multiplier (e.g., 1.5x) is applied due to a simple accident. The plaintiff is credible, but recovery is quick. | $50,000 - $60,000 |

| Moderate Negligence with Ongoing Therapy | A mid-range multiplier (e.g., 3x) is justified. The plaintiff has a solid diagnosis and consistent treatment history. | $80,000 - $100,000 |

| Gross Negligence & Severe PTSD | A high multiplier (e.g., 5x) is used due to reckless conduct. Strong expert testimony supports a permanent life impact. | $120,000 - $150,000+ |

As you can see, the exact same starting number for economic damages can lead to vastly different outcomes. The final number you put in your settlement request has to be backed by this kind of nuanced analysis.

This detailed breakdown is a crucial part of writing a demand letter for personal injury, as it provides the clear justification for the number you're asking for.

Common Questions About Emotional Distress Claims

Even when you feel you have a solid handle on calculating emotional distress, a few tricky questions always seem to pop up. It’s natural. These claims live in a gray area of the law, and insurers are always ready to push back.

Let's walk through some of the most common hurdles you're likely to face.

Can I Claim Emotional Distress Without a Physical Injury?

This is easily one of the most common—and complicated—questions in all of personal injury law. The short answer is, it’s tough, but not impossible.

Most jurisdictions lean on the "impact rule," which basically says you need some kind of physical injury or contact to make a valid claim for emotional distress. The physical harm acts as objective proof that something traumatic actually happened.

But the law recognizes that some experiences are so awful they cause real, severe psychological damage all on their own. This is where the exceptions come in, and they generally fall into two buckets:

- Intentional Infliction of Emotional Distress (IIED): This isn’t for run-of-the-mill bad behavior. We're talking about conduct that is truly extreme and outrageous, done with the specific intent of causing severe emotional pain.

- Negligent Infliction of Emotional Distress (NIED): This is often seen with bystanders who witness a horrific accident involving a close relative. To have a case, you usually need to have been in the "zone of danger"—close enough to the incident that you legitimately feared for your own safety, too.

State laws on this are all over the map. What constitutes NIED in California might get thrown out of court in Texas. Before you even think about pursuing a claim without a clear physical injury, you have to know the specific rules for your jurisdiction.

How Do Insurance Companies Challenge These Claims?

Insurance adjusters are paid to be skeptical, and emotional distress claims are their bread and butter. Their job is to minimize the company's payout, and they have a standard playbook for picking apart your claim.

If you know their tactics ahead of time, you can build a case that’s ready for the fight. You should absolutely expect the adjuster to:

- Blame Pre-existing Conditions: They will dig into your medical records, looking for any history of anxiety, depression, or therapy. Their goal is to argue your current suffering is just a flare-up of an old issue, not a result of their insured's actions.

- Question the Lack of Treatment: If you didn’t rush to a therapist or psychiatrist right away, they'll use it against you. Their logic? If it was really that bad, you would have sought professional help immediately and consistently. This is why getting prompt mental health care is so crucial for documentation.

- Attack Your Calculation: They will tell you your multiplier is wildly inflated or that your per diem rate is completely unrealistic. Expect them to counter with a laughably low figure, which they’ll claim is based on their own "data."

- Use Social Media Against You: This is a big one. Adjusters actively scour Facebook, Instagram, and other social media profiles. That photo of you smiling at a family BBQ or on a weekend trip can be twisted into "proof" that your suffering is exaggerated.

Being ready for these arguments from day one is your best defense. A strong claim is built on consistent medical care, a detailed personal journal, and being mindful of what you post online.

Are There Caps on Emotional Distress Damages?

Yes, unfortunately. Many states have put legal limits, or "caps," on how much money can be awarded for non-economic damages like emotional distress. It's a hot-button political topic, but these caps are a reality that can have a massive impact on your case's value.

The rules vary significantly from one state to another:

- Some states have no caps at all for most personal injury cases.

- Others put a firm ceiling on non-economic damages, often at a set number like $250,000 or $500,000.

- Caps can also depend on the type of case. Medical malpractice claims, for instance, often face much stricter and lower caps than a standard car accident case.

These laws can and do change. A statute that was on the books last year might have been overturned by a court ruling this year. Checking the current laws in your state is non-negotiable, and an experienced attorney will have the most up-to-date information on any caps that could limit your claim's final value.

At Ares, we understand that building a powerful personal injury claim requires meticulous organization and a deep understanding of the case narrative. Our AI-powered platform automates the time-consuming process of reviewing medical records and drafting demand letters, turning stacks of documents into clear, actionable insights. By extracting key facts and creating detailed chronologies in minutes, we empower law firms to build stronger cases, justify higher settlement values, and reclaim countless hours. Learn how you can save time and settle for more at https://areslegal.ai.